By: Dan Hueber –

Relatively stable markets overnight with realistically little more than the weekly crop updates to provide direction. It really would seem a moot point to place much emphasis on crop conditions as how can a plant that is dying look as if it improved? But corn conditions were left unchanged at 61% good/excellent while beans slipped 1% to come in at 59% good/excellent. While this has been discussed ad nauseam this year, it does seem we have a disconnect between ratings and crop forecast. Corn harvest came in slightly under trade expectations at 7%, with beans at 4% but the number of note would have to be the maturity figure for corn. 34% versus 47% on average and 50% last year. With warm temperatures on tap for the next week, frost is by no means high on the scale of concern for the trade, but I have to believe that considering a large swath of the eastern corn belt has been moving towards maturation with very dry conditions, this would not be conducive to good test weight or quality. Dr. Cordonnier currently projects a national yield of 166 for corn and 48 for beans, which I tend to believe is far more realistic than the USDA figures of 169.9 and 49.9. Note that the difference would account for 325.6 million bushels of corn and 168.5 million bushels of beans, even without any harvested acreage adjustments.

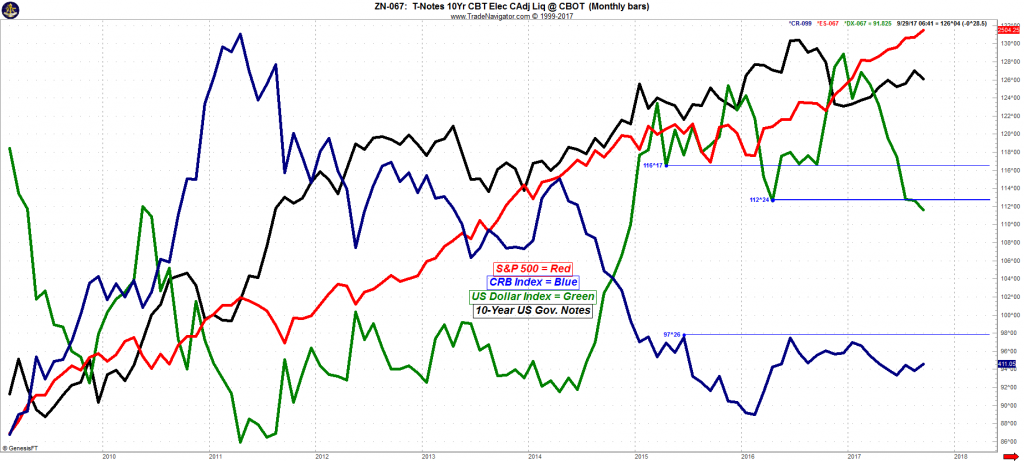

While there may not be any earthmoving ag news around this morning, that is not to say that financials and other markets that have a direct bearing on our businesses are not sitting on pins and needles right now. The topic of concern? The Federal Open Market Committee September meeting that is being conducted today and tomorrow. Unlike with other recent meetings, markets and economists are not so concerned as to if the Fed intends to bump interest rates higher by another 25 basis points (most believe this will happen in December) but rather, what statement or sentiment will they divulge in regards to beginning to unwind the $4.5 balance sheet that was accumulated under the Quantitative Easing stimulus years.

One of the major reasons for the concern is simply because this has never been done before and as Jamie Dimon, CEO of JP Morgan stated earlier this summer, this “could be a little more disruptive than people think.” By allowing this debt to mature, technically the Fed will be tightening the money supply, which in turn could have an impact on business plans, real estate, markets, inflation and of course the U.S. Dollar. Fed Governors are a cautious lot, so no doubt anything they do in the future will be very measured but certainly always breeds caution. I suspect that this is just one more reason as to why we have witnessed large investors stepping away from the equity markets, leaving us poor saps with our 401k’s and IRA’s holding the longs. Expect the comments from Ms. Yellen to be carefully scrutinized after the wrap up tomorrow.