By: Dan Hueber –

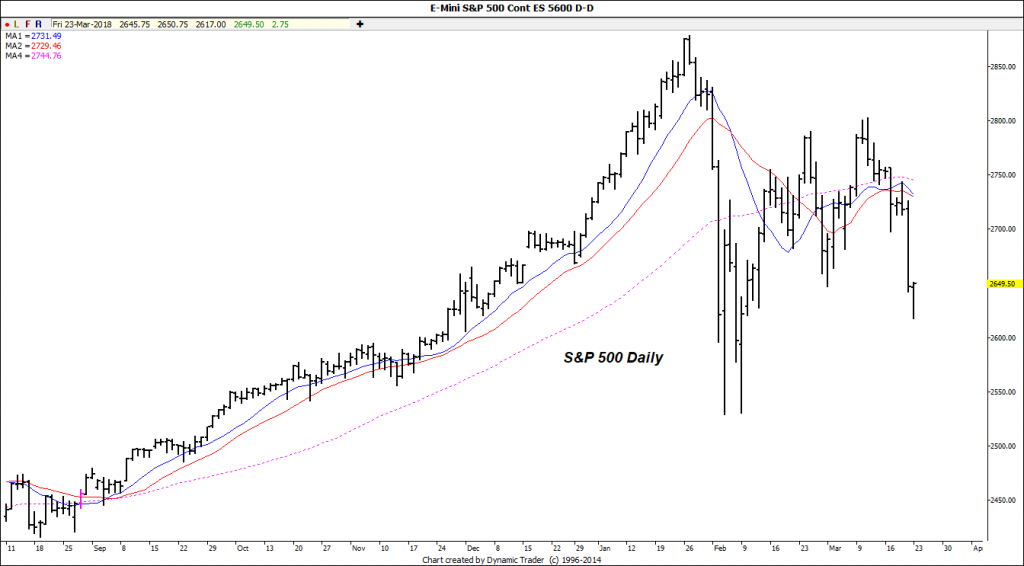

It was almost as if markets wanted to hold out to the very last minute. Hoping against all hope that at the 11th hour, President Trump would reconsider imposing tariffs against China in an effort to, in effect, try and protect US intellectual property rights, but when that turned out to not be the case, the flood gates were open.

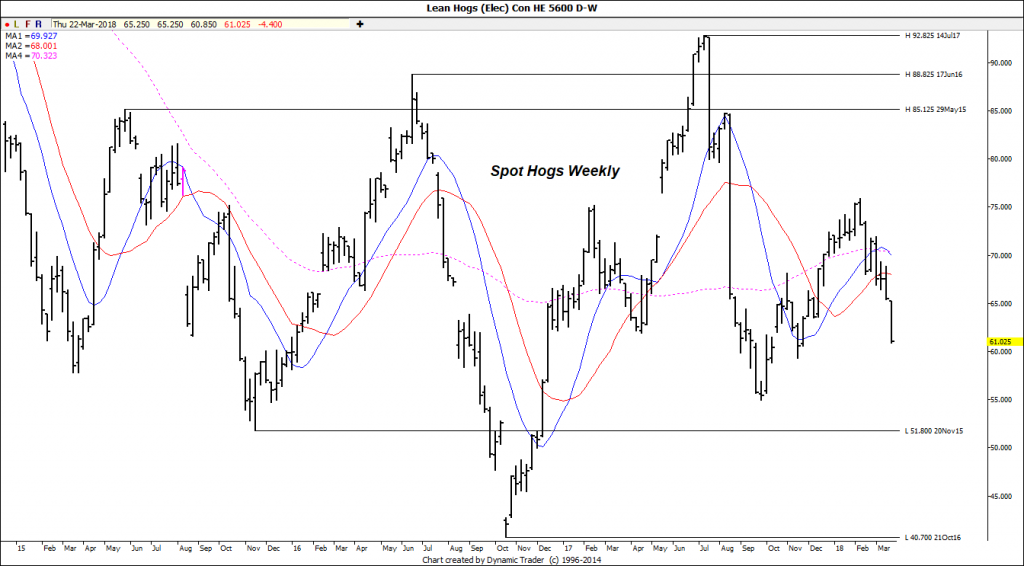

It began in the equity markets as the S&P 500 suffered largest daily loss (2.5%) since February when trade war talk initially heated up, and then overnight that bled over to the foreign equity trade and commodity markets. In a nutshell, there will be imposed at 25% tariff on $60 billion in imports from China. The Chinese response was as would be expected and stating while they do not want a trade war they are prepared to react and were considering an additional 15% tariff on US products including dried fruit, wine and steel pipes and a 25% additional import duty on US pork products and recycled aluminum. Needless to say, the hog market did not receive this as good news.

As I have commented previously, these tariffs, outside of the psychological impact, may not create an enormous impact on US agricultural trade, particularly for soybeans, as logistically China will still need to import from both north and south America. That said, I believe it is the long-term implications that are far more menacing. Particularly when dealing with a nation such as China, who already maintain a much broader perspective of history and long-range planning than we do in the west, it provides them incentive to invest in other regions and resources to secure their needs. We already witnessed this in response to the commodity bubble a decade ago and we should never forget that prior to the 1973 soybean embargo, Brazilian bean production was a mere fraction of ours.

Weekly export sales have now been released, which came as a bit of a letdown for corn and beans. For the week ending March 15th, we sold 1,470,200 MT or 57.9 million bushels of corn. This was towards the lower end of expectations, was 41% below last week and 23% under the 4-week average. Recognize, this was not a terrible number but was the third lowest of the calendar year and is following the highest of the marketing year last week. Top purchasers were South Korea with 449.2k MT, followed by Japan with 263.1k and then Taiwan at 194.6k. For the marketing YTD we have now sold 1.776 billion bushels or 79.8% of the projection of 2.225 billion. Soybean sales fell 40% week over week coming in at 759,000 MT or 27.9 million bushels. China remained on the top of the list with 324.8k MT followed by Taiwan at 82.5k and then Japan with 79.3k. Marketing YTD we now stand at 1.838 billion or 89% of the USDA target of 2.065. Wheat did provide the minor bright spot, with minor being the key word. We sold a total of 265,200 MT or 15.6 million bushels. This was 63% above last week but still 1% below the 4-week average. Top sales were made to Taiwan with 94.3k MT, followed by Nigeria at 49.5k and then unknown destinations at 40.5k. Marketing YTD we now stand at 825.1 million bushels or 89% of the projected 925 million.

On a slightly more positive note to finish out the week, the International Grains Council released updated forecasts yesterday and project a contracting global supply picture. They look for the total grain stocks to drop 46 million tonnes to 560 MMT, with the majority of this occurring in corn which is expected to drop 42 million. They continue to call for a record global bean production mark to be set at 354 MMT but reduced this number 6 MMT from the last due to the issues in Argentina. If we stick with the old philosophy that contacting supplies translate into steady to higher prices, it would suggest we should be headed in the right direction.