By: Dan Hueber –

I wish I had something deep and inciteful or maybe even clever to say about the action in the corn market yesterday but search as I may, I have failed to come up with much. Unless you thought it a good idea to try and build it a little “frost premium” for the late planting progress in the upper Midwest and Plains states, it would seem that most other news would leave traders, well…chilly towards the prospect of a near-term rally. Nevertheless, managed money felt otherwise and piled on at least another 15,000 more contracts, likely taking them north of 200,000 long by a like amount. On one side of the coin, seeing corn or about any commodity post “out of thin air” rallies should not come as a surprise as that is how markets act when you are on the bull side of a cycle. Unlike equity traders who have come to expect, maybe even take for granted such action, we in commodities have nearly forgotten what that is like.

That said, as a whole, many commodities and corn included are still running in place. It is most certainly nice that we are approaching the upper end of the past four-year trading range instead of wallowing down around the low ebb, but regardless, it would still seem that there are enough factors, including the technical side, that would suggest it may be premature to think that the kids are ready to break out of the yard just yet.

Informa released updated acreage estimates yesterday and obviously believe the ag economic outlook has improved enough to attract addition planting. For corn, they are now projecting acreage of 89 million, which would be 1 million above the USDA figure and for beans, a planted number of 89.4 million, which is 400,000 higher than Uncle Sam. Were this correct, using the trend-line yields this would project a possible increase of 159.6 million bushels of corn and 19.2 million beans. While that may not sound all that significant, it would be a 9.5% increase in the projected ending stocks for corn and a 4.7% boost for beans.

To be filed under the category or misery loves company, the price for beans in Brazil has been headed lower and are now below US values in the spot market. Now, one might expect this to sound normal considering they have just harvested a record soybeans crop, but it would appear that the real culprit here is a lack of demand from China. And we thought they had just quit buying US beans. This is not where the similarity in fates stops either as just as in the US, hog producers in China are running deep in the red and in-turn have reduced soymeal consumption/demand in response. Unfortunately, there does not appear to be a quick fix for any of this either and a trader at one of the soy processing companies in China was quoted as saying, “The worst is yet to come, next month will be really bad.”

Currently we have grains higher this morning with soy and products weaker. In the outside marcos we find little to be encouraged about. Energies and metals are weak, the dollar has turned higher once again, and has actually reached into new highs for the year, which in turn has been stimulated by the financial markets.

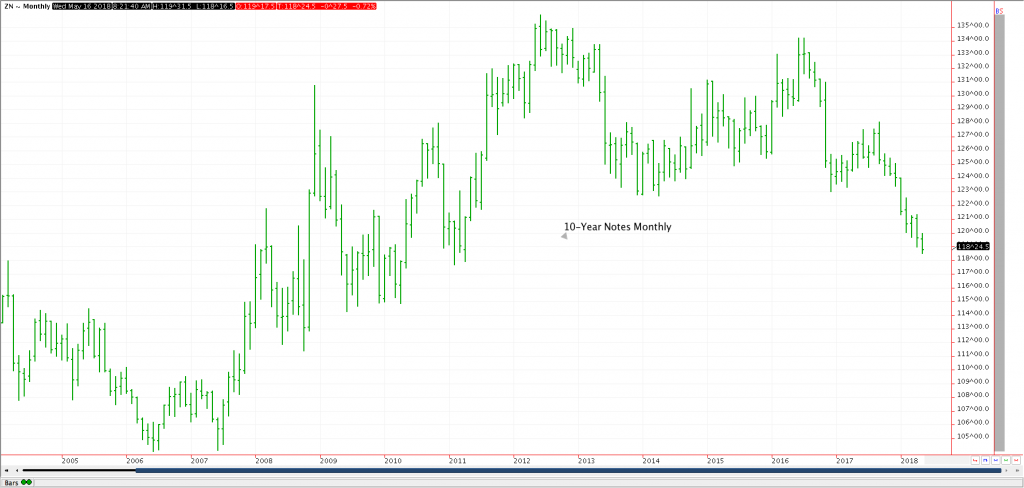

Yesterday, 10-year notes took a dive into lower lows, reaching levels not traded since the spring of 2011. It would appear that the market believes the cost of money will be moving higher for all us in the months ahead.