By: Dan Hueber –

Snow in the northern reaches of this country and rain in the south, virtually assures that we will see little progress with fieldwork or planting in the next few days ahead in the U.S. Are the markets concerned? Obviously not, as this morning we have grains under pressure and beans/meal holding just a bit above water but realistically going nowhere. We are all quite aware of just how rapidly farmers in this nation can plant a crop when conditions become fit, so spring weather concerns are generally pushed aside quickly but we should not lose sight of the potential yield drag the later a crop is planted, which we should be especially mindful with corn this as if there is just 88 million acres planted, there can be no allowance for below trendline yields.

AgRural has provided updates for Brazilian crops over the weekend and estimate that the bean harvest is now 85% complete and the first corn harvest 72% complete. In each case this is off of last year’s pace but historically at this date, beans are normally 84% complete and corn 75%.

There appears to be little discussion of trade tariff’s or tensions this morning, which could be a two-edged sword, but it is worth noting a study that was released late last week by ag economists at Purdue. The study (click here) was commissioned and funded by the US Soybean Export Council and suggests that if tariffs are put in place for four to five years the negative impact would be much greater than many have proposed. Interestingly, the ill effect would almost be equal to both the United States and China, forecasting around a $3 billion hit to the economies of both nations. Here at home though, the largest impact understandably would fall on rural locations. According to the study though, there would be one real beneficiary; Brazil. It is estimated that the they would garner the majority of the 37% cut in US exports to China and provide around a $2.7 billion boost to the economy of that nation. As I have commented previously, it is the long-term implications of these kinds of trade battles that we should truly be concerned with.

Outside of this, the overall news is a bit sparse this morning. Last week managed money added 35,000 contracts to their long position in corn, but sold 5,000 contracts of beans and covered 19,000 contracts from short wheat holdings. Macros are mixed as we have metals a bit higher, energies lower but the U.S. Dollar lower as well. Do note that the dollar has been very stagnant since breaking down in January. While we could still extend lower, from a technical perspective we have reached good retracements and support lines and have long-term indicators sitting in an oversold position, which would appear to have the stage set for a turn higher. If that is the correct, headwinds in the commodities markets will become stronger.

Technical

Wheat – The gap at 4.89 in July wheat remains no longer and it would appear we are poised to cross indicators lower once again. This is not to say that we could not bounce a bit from this low 4.80 level but for now I suspect strength would be fleeting. If correct, I would expect to see this contract make a run back to the 4.60 level and it is not inconceivable to see another stab down against 4.40. The next cycle counts ahead fall on the 26th and then the 7th of May.

Corn – May corn has begun the week with a poke beneath last week’s lows but that appeared to touch off little to no additional selling. That said, this market appears to have crested for now and the daily indicators are right on the cusp of turning lower. If correct, we should be in line for a return trip to the 3.70 level into early May. Cycle counts line up ahead between the 18th and the 24th and then the 30th thru 4th of May.

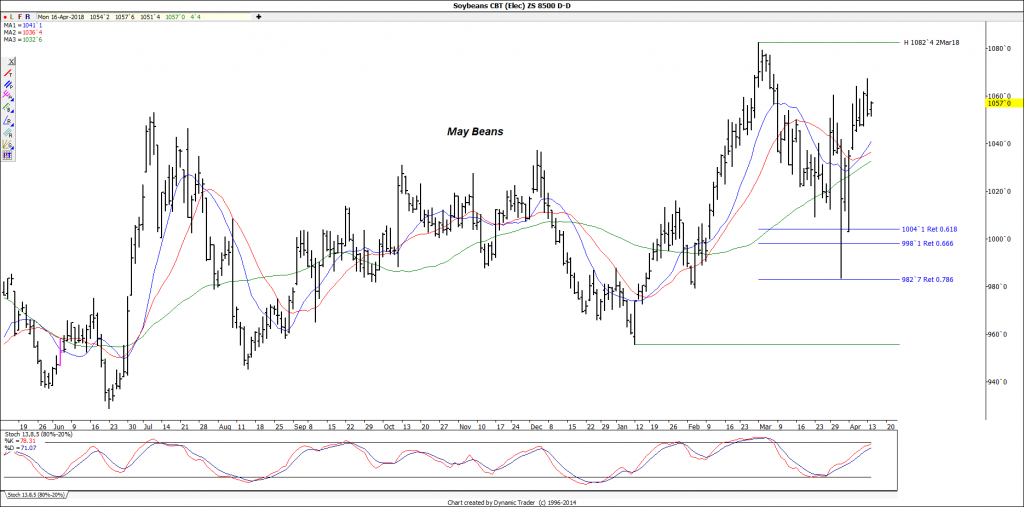

Soybeans – May beans posted what may have been a hook-reversal last Friday but there has not been any follow-through lower this morning. At least not as of yet. As I noted last week, this market is in a big cluster of cycle counts and seeing that we rallied to this time zone and have indicators right at the overbought mark, we should be at or at least extremely close to a reaction high. A close back below 10.46 should provide a confirmation and if accomplished would open the door for a run back down to at least the 10.15/10.00 zone. Cycle counts ahead on the 23rd/24th and then the 4th of May.

Soy Oil – May bean oil has slipped through last week’s lows this morning and bears may be fishing for sell stops, but I suspect they will have temporary success at best. We are right on top of the next cycle count and if beans and meal turn lower, look for buying to return to this market.

Soy Meal – May meal continues to hold in the 380 zone but I suspect will not be able to do so much longer. We already have indicators on the cusp of crossing lower and we sit right on top of cycle counts. A close below 378 should begin to touch off selling and open the door for a swing to at least 350.

Cotton – The 84-cent level has turned out to be tough resistance for May cotton but bulls have not given up the ship just yet. Daily indicators continue to point higher and it would appear we have potential to attack the 85.50/86.00 zone one more time before we exhaust.

Courtesy of The Hightower Report

PORK COMPLEX

Pork production last week up 7.8% last year; $25 basis?

The market continues to rally in spite of the weak cash market as traders clearly anticipate a much stronger than normal cash rally this spring. The CME Lean Hog Index as of April 11th was 52.97, down 5 cents from the previous session and down from 55.27 the previous week. This leaves June hogs at a $24.80 premium to the cash market as compared with the 5-year average premium of just $7.40. This may help limit the upside for June hogs; at least temporarily. June hogs traded to their highest level since March 19th on Friday, continuing a rally that began after the market put in a low on April 4th. In that span of time, the market has gained 785 points and has achieved a 50% retracement of the January-April selloff. Ideas that the Trump Administration’s expressed interest in joining the TPP could improve its bargaining position with China on trade issues has lent a note of optimism to export-based commodities like pork.

There is also a seasonal tendency for pork prices to rally over the next few weeks. The winter storm in the upper Midwest this weekend could delay hog shipments which is somewhat positive but the weather is also a negative for pork demand. The USDA estimated hog slaughter came in at 462,000 head Friday and 91,000 head for Saturday. This brought the total for last week to 2.385 million head, up from 2.335 million the previous week and up 7.1% from last year. Pork production for the week was up 7.8% from last year. USDA pork cutout values, released after the close Friday, came in at $65.52, up 11 cents from Thursday but down from $65.96 the previous week. The Commitments of Traders reports as of April 10th showed Non-Commercial traders were net long 1,768 contracts, a decrease of 5,466 contracts for the week. Non-Commercial and Nonreportable combined traders held a net short position of 12,570 contracts, an increase of 5,049 contracts for the week.

TODAY’S MARKET IDEAS:

The 50% mark of the January to April break comes in at 78.05 and with June hogs already holding a $24.80 premium to the cash market as compared with the 5-year average premium of just $7.40, the upside looks very limited. Support is back at 76.22 and 74.90.

CATTLE COMPLEX

May see some further corrective bounce but supply?

With poor retail demand weather and the outlook for a 10.2% jump in beef production for the second quarter, the short-term fundamentals still look weak. However, with cash at $118, pressing the short-side of June cattle at $103.65 is a difficult task. The market received some support late last week on news that cash live cattle in Texas and Oklahoma traded as high at $118.00, which was $1 higher than the previous week. In the back of traders’ minds is the sharp increase in beef production that is projected for the 2nd quarter. A winter storm moving into the Northern Plains this weekend could raise some concerns about newborn calves. The USDA estimated cattle slaughter came in at 116,000 head Friday and 14,000 head for Saturday. This brought the total for last week to 605,000 head, down from 615,000 the previous week but up 2.7% from a year ago.

Beef production for the week was up 4.5% from last year. USDA boxed beef cutout values were up 36 cents at mid-session Friday and closed 13 cents higher at $212.61. This was down from $214.31 the prior week. The Commitments of Traders reports as of April 10th showed Non-Commercial traders were net long 44,217 contracts, a decrease of 9,608 contracts for the week and the long liquidation selling trend is a short-term bearish force. Non-Commercial and Nonreportable combined traders held a net long position of 30,442 contracts, a decrease of 4,794 contracts for the week. Commodity Index traders held a net long position of 125,355 contracts, a decrease of 4,117 contracts for the week. Cumulative beef export sales for 2018 have reached 359,200 tonnes, up 17.9% from last year’s pace.

TODAY’S MARKET IDEAS:

With the discount and some ideas that the weekend winter storm could have hurt young cattle, we cannot rule out a continued corrective bounce. The chart pattern for June cattle is somewhat positive with 105.17 and 106.67 as resistance. Rallies still look like selling opportunities with 102.10 and 101.12 as support.