By: Dan Hueber –

Anyone who was hoping the USDA to issue something positive on the September crop production report was sorely disappointed today. The corn yield of 169.9 bpa was nearly a bushel and a half above the average estimate and 4/10th of a bushel above last month. At least the figure was still below the highest estimate of 170.9 but no one is going to be able to make a very big silk purse from that sow’s ear. Total production came through at 14.185, which again, was below the highest estimates but was still 150 million above the average and 32 million above last month. Carry-in was just a touch positive at 2.35 billion but the carryout for this new crop year was bumped up 62 million from last month taking it to 2.335 billion. Yes, still a year over year reduction but at 6/10th of a percent, it is hardly worth mentioning. If you think that sounds dour, beans fared even worse. The average yield was pushed up to 49.9 bpa, which was 1.1 above the average estimate and .5 above last month and was even higher than the highest estimate. This equates to a record setting production of 4.431 billion, which is 124 million bushels larger than last year’s record setting figure. Compared with a year ago, the yield is just over 4% lower but of course the 7.2% boost in harvested acreage more than compensates for that. Carry-in was reduced 25 million bushels from last month and at 345 million was even 20 million below the average estimate but the 2017/18 ending stocks number was left unchanged from last month at 475 million. Simple math would suggest that usage must have been pushed higher and indeed, projected exports were bumped up 25 million bushels. Finally, on the domestic front we have wheat, where the USDA made no changes and ending stocks are projected to come in at 933 million bushels compared with 1.184 billion a year ago. While this sounds neutral, the trade was expecting to see a reduction of around 13 million or so. There were a few shifts in the world ending stocks estimates but nothing dramatic.

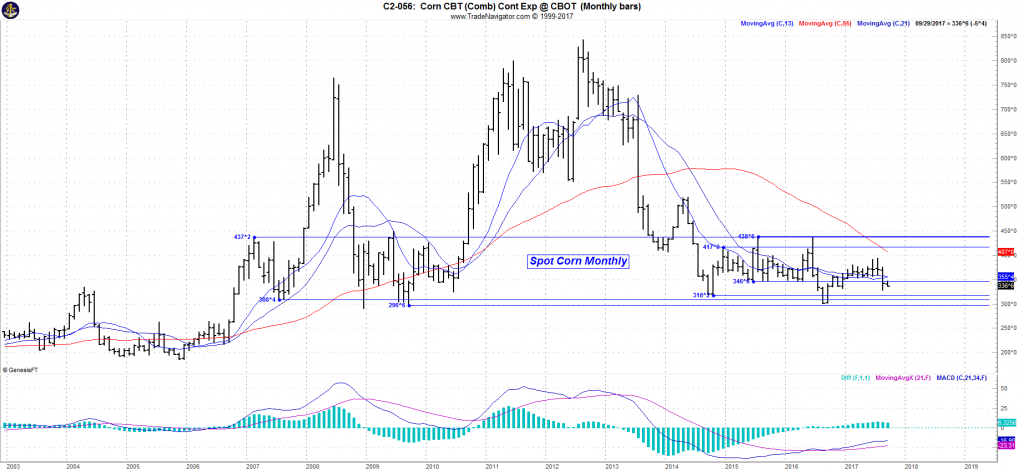

Grain and soy markets have reacted negatively as would be expected, and while none have extended into new lows, we are once again back down against major support levels and seemingly left to continue wandering in this dry and barren zone.

Considering that none of the changes reflect a real increase in the supply compared with recent prior years, one would have to believe downside potential is limited but it does beg the question as to what can bring back out of this zone? While we could speculate that it may be lower numbers once we have entered harvest, possibly a continued decline in the dollar or even a breakdown in the equities markets that brings a flood of value buyers back to ag trade, but for now we can only wait for the dust to settle and begin the process all over again.